What is Coupon Rate?

2.12K

2.12K

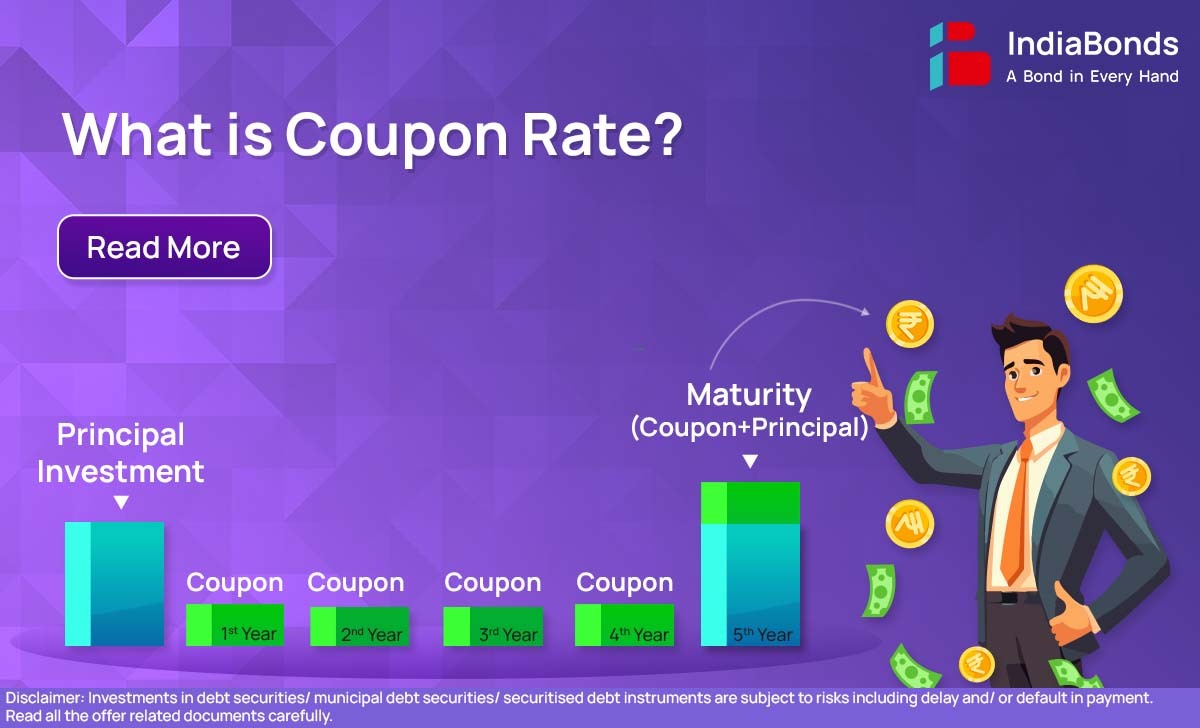

Imagine you’re thinking about lending some money, right? Buying a bond is kind of like that. The company or government you buy the bond from is borrowing from you. Now, for lending them your cash, they give you regular interest payments. The coupon rate is simply the fixed percentage of the original amount you lent (the face value) that they promise to pay you each year. Think of it as your annual “interest reward.”

So, picture this: you buy a bond with an 8% coupon rate and a face value of ₹1,000. That means every year, they’ll send you ₹80 as interest. It’s like getting a predictable little income stream, which is why some folks who don’t like a lot of risk really like bonds – they offer that steady, dependable income.

Working out that coupon rate? Super easy! You just take that yearly “thank you” amount, compare it to the original amount you lent (the face value), and then turn it into a percentage.

Like this:

Coupon Rate = (Annual “Thank You” Money / Original Borrowed Amount) × 100

Using our example:

(₹80 / ₹1,000) × 100 = 8%

Just a few things to keep in mind about this interest rate:

It’s always based on the very first amount you lent, not what the bond might be worth later on.

Usually, this rate is set in stone for the whole time you own the bond – it’s a promise.

If the usual interest rates out in the world are pretty low, a bond that’s offering a higher “thank you” rate looks pretty sweet!

Now, here’s a little twist. The price of a bond can actually do the opposite of what’s happening with general interest rates.

Say everyone suddenly wants to lend money at a higher rate than your bond is paying. Well, your bond’s fixed return might not seem so great anymore, so its price might dip a little to make it more attractive to new buyers. But if interest rates in general drop, suddenly your bond’s steady, higher “thank you” looks really good, and its price might actually go up.

Think of it like a collectible – its value can change depending on what’s popular at the moment.

Sometimes, people get the coupon rate mixed up with the regular interest rate you hear about. But they’re not exactly the same thing. The coupon rate is specific to your bond and stays the same. The general interest rate is more like the heartbeat of the economy, set by banks or just the way things are going, and it affects the terms of new bonds that come out.

And then there’s the yield. The coupon rate is that fixed return, but the yield is the actual return you end up making depending on what you actually paid for the bond.

Let’s go back to our bond:

It gives you an ₹80 interest each year.

If you bought it for ₹1,200 (more than the original ₹1,000), your real return (yield) is less: (₹80 / ₹1,200) × 100 = 6.67%.

But if you managed to buy it for ₹900 (less than the original ₹1,000), your real return (yield) is better: (₹80 / ₹900) × 100 = 8.89%.

So, the coupon is the promised fixed income, but the yield is what you actually pocket based on the price you paid.

There are also other ways bonds can give you returns, like the current yield, the yield to maturity (which figures out your total return if you hold it until the end), and the yield to call (for bonds that might get paid back early).

Some, called zero-coupon bonds, don’t pay any interest along the way. Instead, you buy them for less than they’re worth and get the full amount back at the end. Others, called floating rate bonds, have a interest rate that changes depending on how other interest rates are doing.

So, when you buy a bond, that coupon rate is like your steady paycheck – a predictable amount of income you can count on. If you want to be a savvy bond investor, it’s really key to get your head around what this rate means, how it’s calculated, and how it all connects with how much the bond costs, the usual interest rates out there, and the real return you’re actually going to see (that’s the yield). It’s all about making smart moves so you can build a reliable and stable investment portfolio.

FAQs

1. What is a bond coupon rate?

The bond coupon rate is the fixed percentage of a bond’s face value that investors receive as annual interest payments.

2. How is the bond coupon rate calculated?

The coupon rate is calculated using the formula:

Coupon Rate = (Annual Coupon Payment/Face Value)×100

If you’re wondering an easy way to remember how to calculate coupon rate, simply divide the total annual coupon payment by the bond’s face value and multiply by 100.

3. Is a higher coupon rate always better?

Not necessarily. While a higher coupon rate means more interest earnings, it may also indicate higher risk or credit concerns.

4. How does the coupon rate affect bond pricing?

If market interest rates rise, bond prices tend to fall, making bonds with lower coupon rates less attractive.

5. What is the difference between the coupon rate and yield?

The coupon rate is fixed based on face value, whereas yield changes depending on the bond’s market price.

Disclaimer : Investments in debt securities/ municipal debt securities/ securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully.

2.12K