Apr’23 RBI Policy Highlights

1.43K

1.43K

The RBI’s Monetary Policy Committee (MPC) conducted its monetary policy meeting from April 3-6, 2023.

On the basis of an assessment of the evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today decided to:

- Keep the policy repo rate unchanged at 6.50% consequently the standing deposit facility is unchanged at 6.25% with immediate effect.

- Accordingly, the marginal standing facility (MSF) rate and the Bank Rate remain unchanged at 6.75%

- The reverse repo rate under the LAF stands unchanged at 3.35%.

- The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

- These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4% within a band of +/- 2%, while supporting growth.

Part A: RBI’s Policy decision Rationale:

1. Inflation

CPI headline inflation rose from 5.7% in December 2022 to 6.4% in February 2023 on the back of higher inflation in cereals, milk and fruits and slower deflation in vegetables prices. Fuel inflation remained elevated, though some softening was witnessed in February due to a fall in kerosene (PDS) prices and favorable base effects. Core inflation (i.e., CPI excluding food and fuel) remained elevated and was above 6% in January’23-February’23. The moderation observed in inflation in clothing and footwear, and transportation and communication was largely offset by a pick-up in inflation in personal care and effects and housing.

The MPC expects CPI outlook to be shaped by several factors such as:

- The expectation of a record rabi food grains production bodes well for the food prices outlook.

- The impact of recent unseasonal rains and hailstorms, however, needs to be watched. Milk prices could remain firm due to high input costs and seasonal factors.

- Global financial market volatility has surged, with potential upsides for imported inflation risks.

- Easing cost conditions are leading to some moderation in the pace of output price increases in manufacturing and services, as indicated by the Reserve Bank’s enterprise surveys.

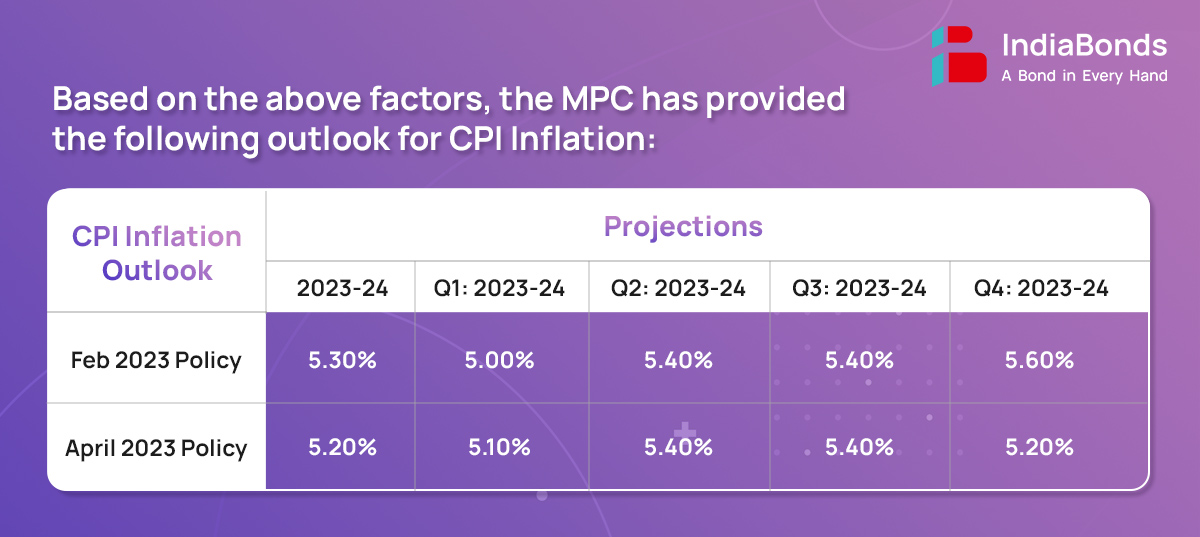

- Taking into account these factors and assuming an annual average crude oil price of USD 85 per barrel and a normal monsoon, CPI inflation is projected at 5.20% for 2023-24, with Q1 at 5.10%, Q2 at 5.40%, Q3 at 5.40% and Q4 at 5.20%, and risks evenly balanced.

2. Growth

Domestic Economic activity remained resilient in Q4. Rabi food grains production is expected to increase by 6.20% in 2022-23. The index of industrial production (IIP) expanded by 5.20% in January 2023 while the output of eight core industries rose even faster by 8.90% in January 2023 and 6.0% in February 2023, indicative of the strength of industrial activity. In the services sector, domestic air passenger traffic, port freight traffic, e-way bills and toll collections posted healthy growth in Q4, while railway freight traffic registered a modest growth. Purchasing managers’ indices pointed towards sustained expansion in both manufacturing and services in March.

The MPC expects real GDP to be based on the following factors:

- A good rabi crop should strengthen rural demand, while the sustained buoyancy in contact-intensive services should support urban demand.

- According to the RBI’s surveys, businesses and consumers are optimistic about the future outlook. The external demand drag could accentuate, given slowing global trade and output.

- Protracted geopolitical tensions, tight global financial conditions and global financial market volatility pose risks to the outlook.

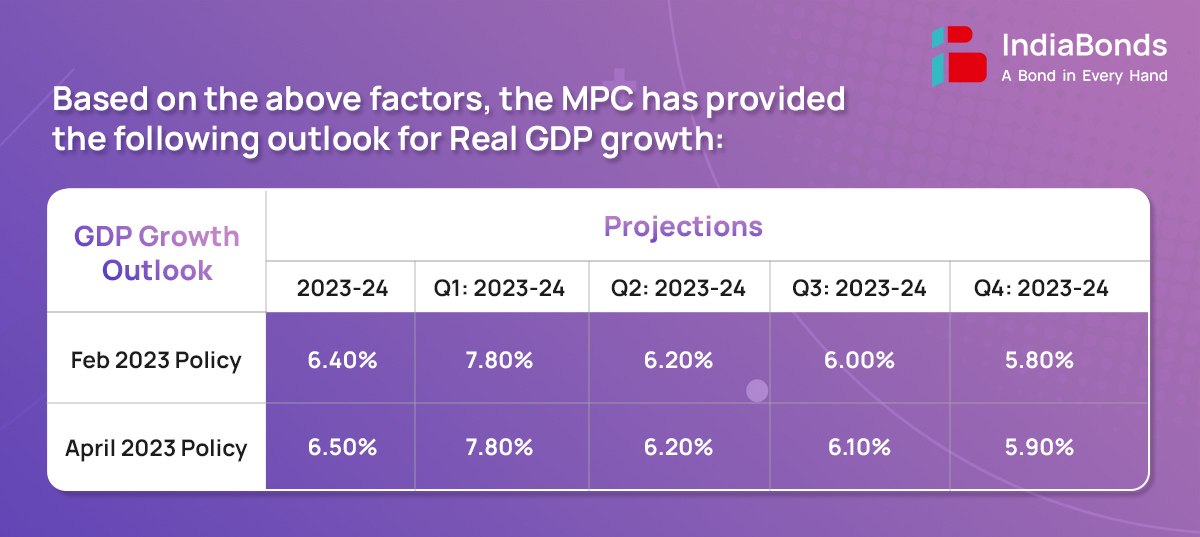

- Taking all these factors into consideration, real GDP growth for 2023-24 is projected at 6.50% with Q1:2023-24 at 7.80%; Q2 at 6.20%; Q3 at 6.10%; and Q4 at 5.90%, with risks evenly balanced.

3. Liquidity

- The average daily absorption under the LAF moderated to Rs.1.4 lakh crore during February-March from an average of Rs.1.6 lakh crore in December-January.

- During 2022-23, money supply expanded by 9.0% and non-food bank credit rose by 15.4 per cent. India’s foreign exchange reserves were placed at USD 578.4 billion as on March 31, 2023.

4. Global Economy

Global economic activity remains resilient amidst the persistence of inflation at elevated levels, turmoil in the banking system in some advanced economies, tight financial conditions and lingering geopolitical hostilities. Recent financial stability concerns have triggered risk aversion, flights to safety and heightened financial market volatility. Sovereign bond yields fell steeply in March on safe haven demand, reversing the sharp increase in February 2023 over aggressive monetary stances and communication. Equity markets have declined since the last MPC meeting and the US dollar has pared its gains. Weakening external demand, spillovers from the banking crisis in some AEs, volatile capital flows and debt distress in certain vulnerable economies weigh on growth prospects.

Part B: Key Statements on Developmental and Regulatory Policies:

1. Developing an Onshore Non-deliverable Derivatives Market

Banks in India which operate International Financial Services Centre (IFSC) Banking Units (IBUs) were permitted to transact in INR Non-deliverable foreign exchange derivative contracts (NDDCs) with non-residents and with each other with effect from June 1, 2020. It has been decided to permit banks with IBUs to offer INR NDDCs to resident users in the onshore market. These banks will have the flexibility of settling their NDDC transactions with non- residents and with each other in foreign currency or in INR while transactions with residents will be mandatorily settled in INR.

2. Enhancing Efficiency of Regulatory Processes

The application and approval processes for various entities are required to obtain license / authorization to carry out activities regulated by RBI. In the Union Budget for 2023-24 has announced the need to simplify, ease and reduce cost of compliance by financial sector regulators within laid down time limits to decide the applications under various regulations. It has, therefore, been decided to develop a secured web based centralized portal named as ‘PRAVAAH’ (Platform for Regulatory Application, Validation And Authorizations) which will gradually extend to all types of applications made to RBI across all functions.

3. Development of Centralized Web portal for Public to Search Unclaimed Deposits

The deposits remaining unclaimed for 10 years in a bank are transferred to the “Depositor Education and Awareness” (DEA) Fund maintained by the Reserve Bank of India. RBI has been taking various measures to ensure that newer deposits do not turn unclaimed and existing unclaimed deposits are returned to the rightful owners or beneficiaries after following due procedure. On the second aspect, banks display the list of unclaimed deposits on their website. RBI has decided to develop a web portal to enable search across multiple banks for possible unclaimed deposits based on user inputs. The search results will be enhanced by use of certain AI tools.

4. Grievance Redress Mechanism relating to Credit Information Reporting by Credit Institutions and Credit information provided by Credit Information Companies

Increase in customer complaints regarding credit information reporting and the functioning of credit information companies (CICs), it has been decided to put in place a comprehensive framework for strengthening and improving the efficacy of the grievance redress mechanism and customer service provided by the credit institutions (CIs) and CICs. For this purpose, the CICs have been brought under the aegis of the Reserve Bank Integrated Ombudsman Scheme (RB-IOS). It is also proposed to put in place the following measures: a compensation mechanism for delayed updation/rectification of credit information; a provision for SMS/ email alerts to customers when their credit information are accessed from CICs; a timeframe for ingestion of data received by CICs from Credit Institutions; and disclosures relating to number and nature of customer complaints received on the website of CICs.

5. Operation of Pre-Sanctioned Credit Lines at Banks through the UPI

Unified Payments Interface (UPI) is a robust payments platform supporting an array of features and handles 75% of the retail digital payments volume in India. RuPay credit cards were permitted to be linked to UPI. At present, UPI transactions are enabled between deposit accounts at banks, sometimes intermediated by pre-paid instruments including wallets. It is now proposed to expand the scope of UPI by enabling transfer to / from pre-sanctioned credit lines at banks, in addition to deposit accounts.

The next meeting of the MPC is scheduled during 06th – 08th June’23.

Disclaimer: Investments in debt securities/ municipal debt securities/ securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully.

1.43K