April 2026 Monetary Policy Highlights

543

543

The RBI’s Monetary Policy Committee (MPC) conducted its monetary policy meeting from April 6 to April 8, 2026.

On the basis of an assessment of the evolving macroeconomic situation, the Monetary Policy Committee (MPC) made the following announcements:

- The MPC unanimously decided to maintain the repo rate at 5.25%. Consequently, the SDF rate is maintained at 5.00%.

- The Marginal Standing Facility (MSF) rate and the Bank Rate were also kept unchanged at 5.50%.

- MPC has also decided to keep the stance unchanged at Neutral.

Part A: RBI’s Policy Decision Rationale:

1. Inflation

In January-February, headline inflation continued to remain below target (2.7% and 3.2%, respectively), with food group recording inflation vis-a-vis a deflation in the previous four months. Inflation in fuel items was modest. Core inflation was at 3.7% and the underlying price pressures benign, as evident from the much lower core inflation excluding precious metals at 2.1%. Food price outlook remains comfortable in the near term with robust rabi production, adequate reservoir levels and comfortable buffer stocks of food grains. Recent spikes in energy prices due to the conflict have emerged as a risk. Although retail prices of petrol and diesel have remained unchanged so far, the pass-through of higher global energy prices has resulted in some price increases in a few other fuel items.

The MPC expects CPI outlook to be shaped by several factors such as:

- Robust rabi production, adequate reservoir levels and comfortable buffer stocks of food grains.

- Volatility in the global energy prices owing to the conflict in the West Asia.

- The likely emergence of El Niño conditions could pose a risk.

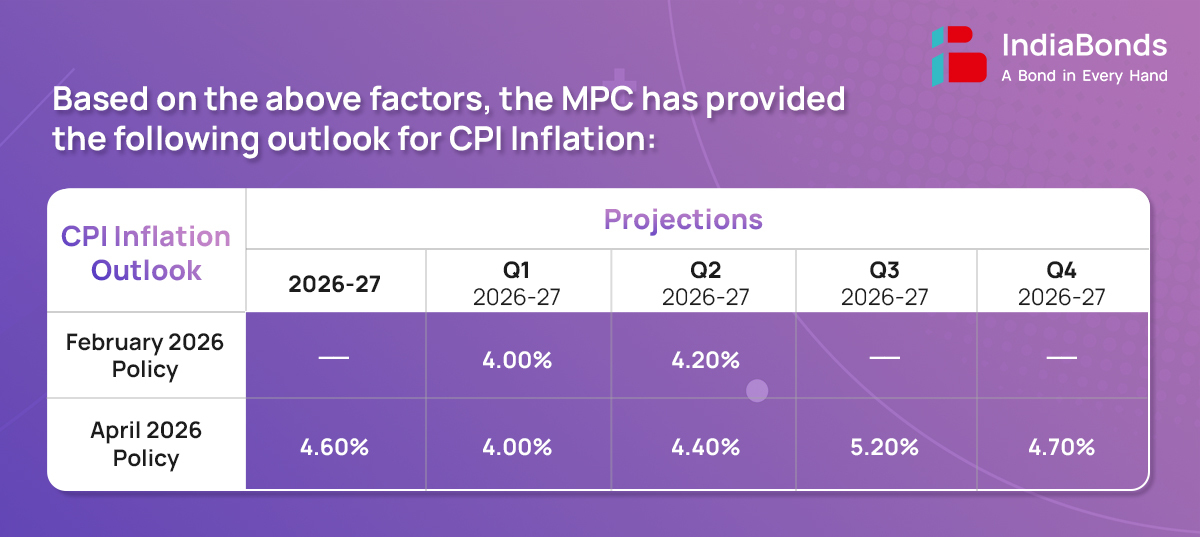

- Considering all these factors, CPI inflation for 2026-27 is projected at 4.6% with Q1 at 4.0%; Q2 at 4.4%; Q3 at 5.2%; and Q4 at 4.7%.

- Core inflation is projected at 4.4% for FY27 and, excluding precious metals, it is even lower indicating that underlying inflation pressures are expected to remain contained

2. Growth

As per the new GDP series (base year 2022-23), the Indian economy’s real GDP growth for 2025-26 is estimated at 7.6%. Elevated energy and other commodity prices, as also shocks to availability of inputs due to disruptions in the Strait of Hormuz are likely to impact growth in 2026-27. Healthy balance sheets of financial institutions and corporates are actively propelling the growth momentum along with growth push policy implementation from the government. Disruptions in energy markets, fertilizers and other commodities may adversely impact industry, agriculture and services, reducing domestic output. On the other hand, weaker global demand and financial conditions are expected to reduce potential export output of the economy based on high freight costs, insurance premiums and muted demand until a stable and permanent solution and restoration of global supply chain and logistics is implemented across the global markets.

The MPC expects real GDP to be based on the following factors:

- Agricultural activity will be supported by healthy reservoir levels, robust rabi sowing.

- Higher input costs in industries due to supply chain disruptions and higher war risk premium.

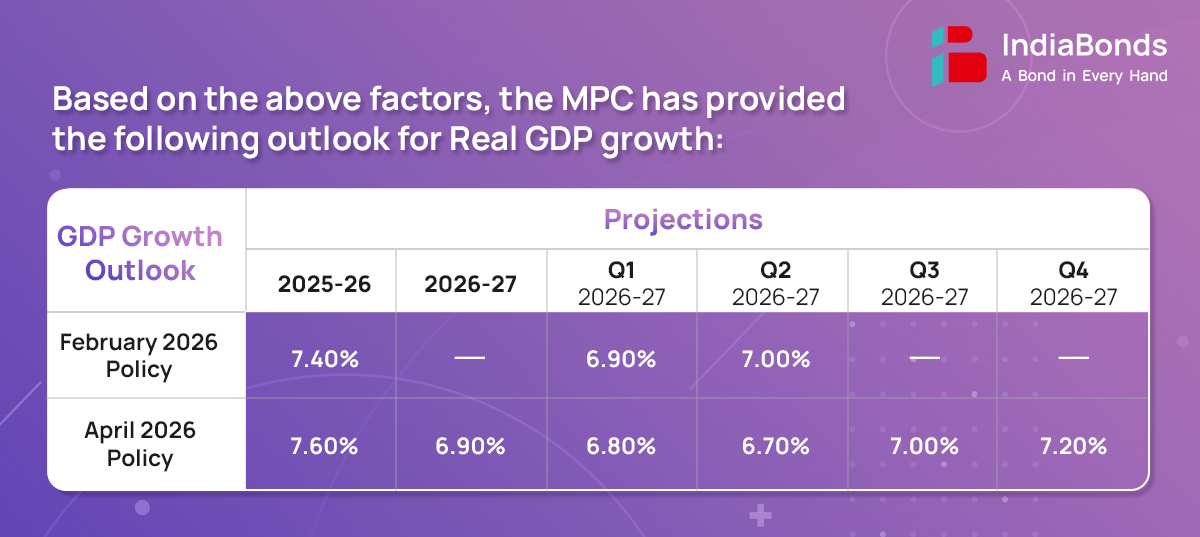

- Taking all these factors into consideration, real GDP growth for 2026-27 is projected at 6.9%, with Q1 at 6.8%; Q2 at 6.7%; Q3 at 7.0%; and Q4 at 7.2%.

3. Liquidity

- System liquidity, as measured by the net position under the Liquidity Adjustment Facility (LAF), stood at an average daily surplus of ₹2.3 lakh crore since the last MPC meeting.

- Since then, call rate has traded in the lower half of the corridor except towards end-March. Short term money market rates, especially those of commercial papers and certificates of deposit, remained elevated.

- G-Sec yields remained largely range-bound with a softening bias in February but firmed up thereafter on account of the ongoing conflict, hardening global yields and the rise in energy prices.

- Going ahead, RBI will continue to be proactive and pre-emptive in liquidity management and ensure sufficient liquidity in the banking system to meet the productive requirements of the economy.

4. Global Economy

Global growth faces increasing downside risks as the sharp rise in energy prices and shortages of inputs for various industries have stoked inflation fears and pushed up the geopolitical risk premium in oil markets. Heightened uncertainty precipitated by the ongoing conflict is weighing on the outlook. Safe-haven flows have exerted depreciation pressure on currencies of major economies as the US dollar has strengthened. While commodity prices, such as of metal and gold, have moderated, financial markets have become more volatile. Equities registered a broad-based correction.

Part B: Key Statements on Developmental and Regulatory Policies:

1. Review of guidelines for inclusion of Quarterly Profits in Capital to Risk-weighted Assets Ratio (CRAR) computation

Commercial banks will soon be allowed to include quarterly net profits in their CRAR (Capital to Risk-Weighted Assets Ratio) without meeting the current “25% NPA provision deviation” rule. The RBI proposes to remove this restriction, with draft guidelines forthcoming for public feedback.

2. Development of Term Money Market

To improve liquidity and monetary policy transmission, the RBI has expanded the term money market. It will now allow non-bank participants to join banks and Primary Dealers. Additionally, borrowing limits for standalone Primary Dealers will be increased. Revised directions are forthcoming.

3. Simplifying the onboarding process of MSMEs in Trade Receivables Discounting System (TReDS)

RBI proposes removing mandatory due diligence for MSMEs onboarding the TReDS platform. This follows previous expansions, like including insurance companies, to accelerate working capital access. A comprehensive review of TReDS instructions is underway, with draft directions for public consultation coming soon.

4. Review of Guidelines on Investment Fluctuation Reserve (IFR)

The RBI proposes to eliminate the Investment Fluctuation Reserve (IFR) requirement for commercial banks, as existing market risk capital charges already provide sufficient buffers. Guidelines for SFBs, PBs, and RRBs will also be revised to harmonize rules and improve operational consistency. Draft directions for public comment are forthcoming.

5. Review of matters placed before the Boards of the Banks

The RBI is rationalizing board-level reporting requirements to help bank boards focus on strategy and risk governance. While boards currently follow seven RBI themes, the new proposal aims to reduce mandatory reporting burdens by reviewing existing instructions. Draft directions for these streamlined guidelines will be issued shortly.

6. Consolidation of Supervisory Instructions

Following its 2025 regulatory consolidation, the RBI has now streamlined supervisory instructions. It has condensed thousands of guidelines into 64 functional Master Directions to reduce compliance costs and enhance clarity. Drafts are now live on the RBI website for public feedback.

The next meeting of the MPC is scheduled for June 3 – 5, 2026.

Disclaimer : Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities, municipal debt securities/securitised debt instruments are subject to credit risks, market risks and default risks including delay and/or default in payment. Read all the offer related documents carefully.

.

543