Download IndiaBonds App

400K+ Downloads

December 2025 Monetary Policy Highlights and Rationale

6.99K

6.99K

The RBI’s Monetary Policy Committee (MPC) conducted its monetary policy meeting from December 3 to December 5, 2025.

On the basis of an assessment of the evolving macroeconomic situation, the Monetary Policy Committee (MPC) made the following announcements:

- The MPC unanimously reduced the repo rate by 25 bps to 5.25%. Consequently, the SDF rate was revised downward to 5.00%.

- The Marginal Standing Facility (MSF) rate and the Bank Rate were also revised downward by 25 bps to 5.50%.

- The MPC has unanimously decided to maintain a neutral stance.

Part A: RBI’s Policy decision Rationale:

Inflation

The headline inflation has declined sharply since the Oct’25 policy, reaching historically low levels. Average CPI inflation eased to 1.7% in Q2 FY26, breaching the lower tolerance band of 2% for the first time under the flexible inflation targeting framework, and fell further to 0.3% in October 2025, driven by a sharp correction in food prices and subdued price pressures across major components. Global inflation trends remain divergent, with advanced economies experiencing above-target inflation, while emerging markets show contained pressures. Core inflation softened marginally in Q2 FY26 and is expected to remain in range. Excluding precious metals, underlying inflation pressures are weaker. Both headline and core inflation are projected at or below 4% through H1 FY27.

The MPC expects CPI outlook to be shaped by several factors such as:

- Healthy kharif output, ample reservoir levels, and sufficient stocks of food grains are likely to keep food inflation under control.

- Core inflation is projected to remain marginally above 4% for FY26, while weather events and geopolitical risks pose upside pressures.

- Satisfactory southwest monsoon progression, combined with adequate soil measurement treatment, supports stable food prices in the near term. Risk to inflation remains contained.

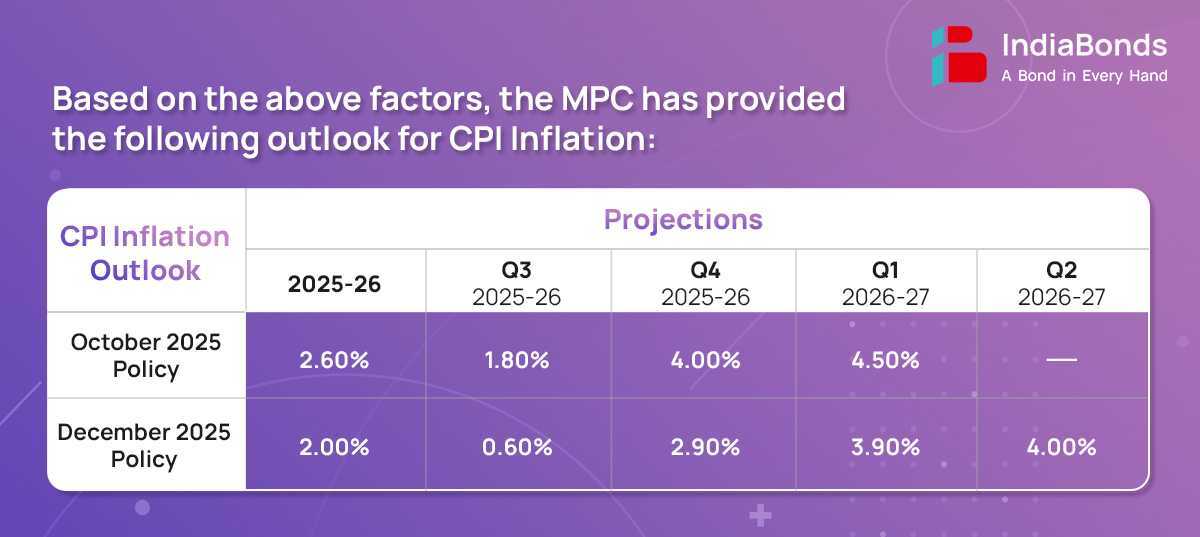

- Assuming a normal monsoon, the CPI inflation for the FY26 is projected at 2.0% with Q3 at 0.6%, Q4 at 2.9%, Q1 FY27 at 3.9% and Q2 FY27 at 4.0%.

Growth

Real GDP grew 8.2% in Q2 FY26, the highest in six quarters, supported by resilient domestic demand amid global trade and policy uncertainties. Real GVA expanded 8.1%, driven by robust industrial and services sectors. H1 FY26 activity benefited from GST and income tax rationalization, softer crude prices, front-loaded government capital expenditure, and accommodative monetary conditions. Festival consumption boosted domestic demand, with rural demand remaining strong and urban demand recovering steadily. Investment activity was healthy, aided by private investment, and higher non-food bank credit. Agriculture grew on strong kharif and rabi prospects, while manufacturing and services remained steady. External sector resilience was supported by strong remittances and FDI, despite merchandise export moderation. Foreign exchange reserves stood at USD 686.2 billion, covering over 11 months of imports.

The MPC expects real GDP to be based on the following factors:

- Robust services sector growth, steady employment, and GST rationalization continue to support the domestic demand and investment expansion. Agricultural and rural demand are supported by above-normal monsoon.

- High capacity utilization, favorable financial conditions, and rising domestic consumption are expected to sustain investment momentum across sectors.

- External demand faces headwinds from trade and tariff uncertainties, while geopolitical tensions and global market volatility pose risks, keeping investor sentiment cautious and potentially affecting exports and growth.

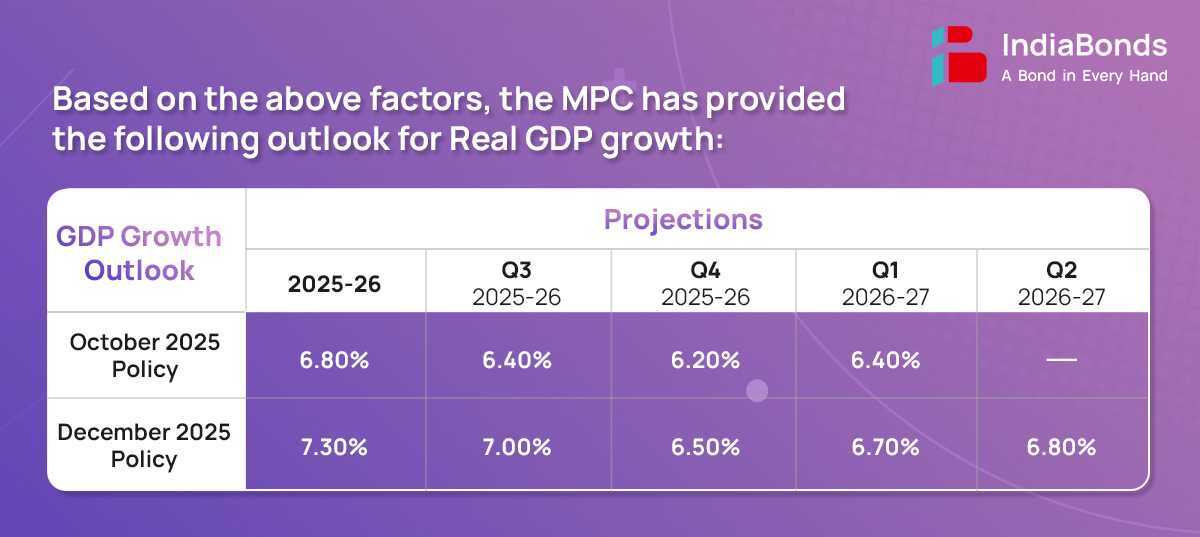

- Taking all these factors into account, real GDP growth for FY26 is projected at 7.30%, with Q3 at 7.00%, Q4 at 6.50%, Q1 FY27 at 6.70% and Q2 FY27 at 6.80%.

Liquidity

- System liquidity has remained in surplus, averaging Rs. 1.5 lakh crore per day since the last MPC meeting, supported by RBI measures.

- RBI will conduct OMO purchases of Rs. 1 lakh crore in two tranches (11th & 18th Dec’25), along with a 3-year USD/INR Buy-Sell swap of USD 5 billion on 16th Dec 2025, injecting durable liquidity into the system.

- Following the cumulative 100 bps repo rate cut, WALR on fresh rupee loans fell 69 bps, outstanding loans 63 bps, while fresh and outstanding deposit rates declined 105 bps and 32 bps, reflecting broad-based transmission.

- Scheduled OMO’s will provide durable liquidity, while LAF operations (VRR/VRRR) manage short-term liquidity to align the weighted average call rate with the policy repo rate, allowing simultaneous injection and absorption of liquidity.

- Going forward, RBI will continue ensuring sufficient durable liquidity, closely monitoring system needs from currency, forex operations, and reserve maintenance.

Global Economy

Global growth has been relatively strong, though geopolitical tensions and trade uncertainties persist. Inflation remains above target in advanced economies but contained in emerging markets, allowing accommodative policy. Equity markets are volatile due to AI optimism, high valuations, and divergent central bank policies. Uncertainty eased after the US shutdown and trade progress, while US Dollar has strengthened with volatile US treasury yields.

The next meeting of the MPC is scheduled from February 4-6, 2026.

6.99K

CIN: U67100MH2008PTC178990

SEBI Registration No.: INZ000311637

NSE Member ID - Debt Segment: 90316

BSE Member ID - Debt Segment: 6811

Caution : Beware of fraudsters and impersonators misusing the name of IndiaBonds. Always verify communications and transactions through our official website www.indiabonds.com and mobile application only. Click here for Advisory and Safety Tips.