June 2026 Monetary Policy Highlights and Rationale

280

280

The RBI’s Monetary Policy Committee (MPC) conducted its monetary policy meeting from June 3 to June 5, 2026.

On the basis of an assessment of the evolving macroeconomic situation, the Monetary Policy Committee (MPC) made the following announcements:

– The MPC unanimously decided to maintain the repo rate at 5.25%. Consequently, the SDF rate is maintained at 5.00%.

– The Marginal Standing Facility (MSF) rate and the Bank Rate were also kept unchanged at 5.50%.

– MPC has also decided to keep the stance unchanged at Neutral.

Part A: RBI’s Policy Decision Rationale:

1. Inflation:

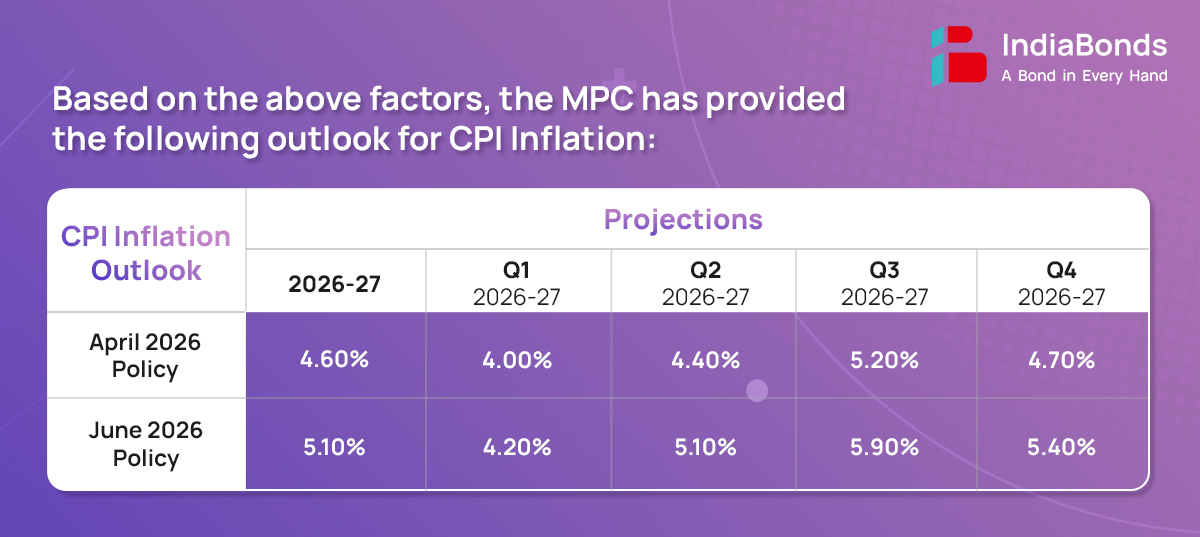

In March-April, headline inflation continued to remain below target (3.4% and 3.5%, respectively), with food outlook remaining unpredictable due to weather impacts from El-Nino. Core inflation was at 3.7% for March-April. Food price outlook remains comfortable in the near term with a watch on developing weather patterns as MPC decided to wait for more clarity to emerge on south-west monsoon forecast and El Niño. Recent spikes in energy prices due to the conflict pushed input costs and freight tick higher, adding to inflationary pressures. With Oil prices gradually elevating in the broader economy, inflation is expected to increase resulting in acting as a drag for domestic/household demand. CPI inflation for 2026-27 is projected to be at 5.1.

The MPC expects CPI outlook to be shaped by several factors such as:

- Volatility in the global energy prices owing to the conflict in the West Asia.

- El-Nino and sub-par south western monsoon.

- Inflationary pressures from elevated crude and resultant business input costs.

- Considering all these factors, CPI inflation for 2026-27 is projected at 5.1% with Q1 at 4.2 per cent; Q2 at 5.1 per cent; Q3 at 5.9 per cent; and Q4 at 5.4 per cent.

- Core inflation is projected at 4.7 per cent for 2027, compared to previously declared 4.4 per cent due to weather impacts, energy costs and rise in imported inflation.

2. Growth

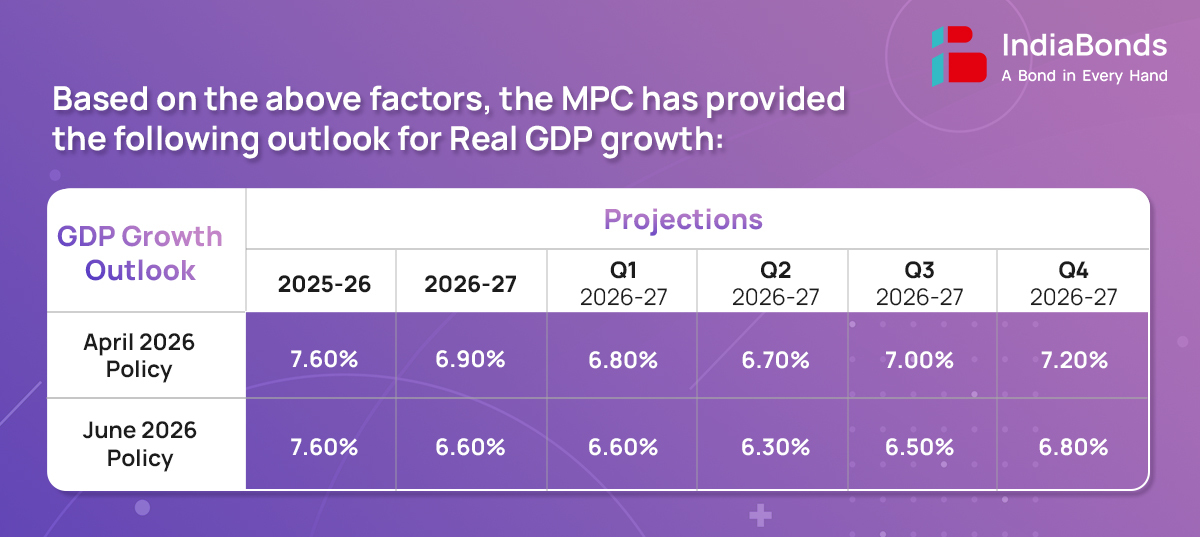

As per the second estimate of National Statistics organization (NSO), the Indian economy’s real GDP growth for 2025-26 is estimated at 7.6%. Global disruptions due to the middle east conflict and significant rise in input costs dragged the growth pace but robust domestic demand and private consumption, along with healthy balance sheets of financial institutions with positive outcome from manufacturing and services sectors activity aided in growth. Disruptions in energy markets, supply chains, increased freight and insurance based risk premiums increased business input costs. Also, weaker global demand and financial conditions are expected to reduce potential export output of the economy based on conflict’s economical spillovers and muted demand until a stable and permanent solution and restoration of global supply chain and logistics takes shape for the broader global economy.

The MPC expects real GDP to be based on the following factors:

- Agricultural activity will be supported by healthy reservoir levels though unpredictability in monsoon and imminent effects of El-Nino are under watch.

- Higher input costs in industries due to elevated energy prices and higher insurance premiums.

- Taking all these factors into consideration, GDP growth estimate for FY27 has been revised downwards to 6.6% from earlier 6.9%.

3. Liquidity

- System liquidity, as measured by the net position under the Liquidity Adjustment Facility (LAF), stood at an average daily surplus of ₹2.6 lakh crore since the last MPC meeting.

- Since then, call rate has traded within the policy corridor. Short term money market rates, especially CPs and CDs moderated before coming under pressure in May.

- G-Sec yields eased in April following the ceasefire announcement in West Asia but firmed up in May. Transmission in the credit market has moderated during March-April with some hardening in deposit and lending rates.

- Going ahead, RBI will continue actively manage and ensure sufficient liquidity in the banking system to aid policy transmission and promote growth.

4. Global Economy

The spillovers from the US-Iran conflict has impacted global economy through various growth drags like elevated energy costs, protective war-risk premiums and muted overall demand. Though among all these factors, Indian economy has shown signs of resilience owing to robust domestic demand and overall growth in business activity. Recent manufacturing and services data indicates sustained growth momentum though input costs for businesses ticked higher due to external spillovers. With commodity prices impacted across different key economies, external demand has recorded a slide as compared to previous estimations. With a potential peace-resolution in works, expectations of corrections in energy prices and higher imported costs is expected to play out in the upcoming months.

Part B: Key Statements on Developmental and Regulatory Policies:

1. Capital gains tax on foreign investment in Indian bonds scrapped

To boost foreign capital inflows, long-term capital gains tax on investments by foreign institutional investors (FIIs) in government securities has been scrapped, At present, foreign investors are subject to 12.5% long-term capital gains tax on listed equities and bonds held for more than one year. Interest earned on government securities is also taxed through a 20% withholding levy.

2. Increased access to the G-sec market for Foreign Investors

RBI expanded the range of government bonds that foreign investors can buy without investment restrictions by including all new issuances of 15-year, 30-year and 40-year tenor Government securities under the fully accessible route. Limits pertaining to short-term investment, concentration and individual securities on FPI investment under the General Route have been removed.

3. Investment restrictions on NRIs, OCIs and PROIs Eased

Limits for Investment by NRIs and Overseas Citizen of India (OCIs) in equity instruments traded on the stock market without SEBI registration have been increased, further the same facility is being extended to all individual persons Resident Outside India (PROIs) at par with NRIs and OCIs.

4. Concessional Forex Swap to PSUs to encourage ECBs

RBI to provide a facility of concessional forex swap till 30th Sep 2026 to incentivize External Commercial Borrowings (ECBs) by Public Sector Undertakings (PSUs), The facility is expected to lower hedging costs and make overseas borrowings more attractive, attracting higher foreign inflows and to ease pressure on the rupee.

5. RBI to bear full hedging cost on fresh FCNR(B) deposits

RBI has announced a special measure to encourage foreign currency inflows, offering to bear the full hedging cost on fresh 3-5 year Foreign Currency Non-Resident (Bank) deposits mobilised by banks until September 30, 2026. Under the scheme, authorised dealer (AD) banks raising fresh FCNR(B) deposits will receive RBI support for the entire hedging cost, making such deposits more attractive and helping banks garner additional foreign currency funds from non-resident Indians.

6. Export proceeds realisation period restored to 9 months

The RBI restored the export proceeds realisation period to nine months from 15 months. This means exporters will again have to bring back export earnings within nine months. The move shortens the earlier flexibility available to exporters but can help improve the timing of foreign exchange inflows into the country. By reducing the period for realising export proceeds, the central bank is also trying to ensure that foreign exchange earnings return to the system faster.

The next meeting of the MPC is scheduled for August 3 – 5, 2026.

Disclaimer : Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities, municipal debt securities/securitised debt instruments are subject to credit risks, market risks and default risks including delay and/or default in payment. Read all the offer related documents carefully.

280