Download IndiaBonds App

400K+ Downloads

Union Budget FY 26-27

1.31K

1.31K

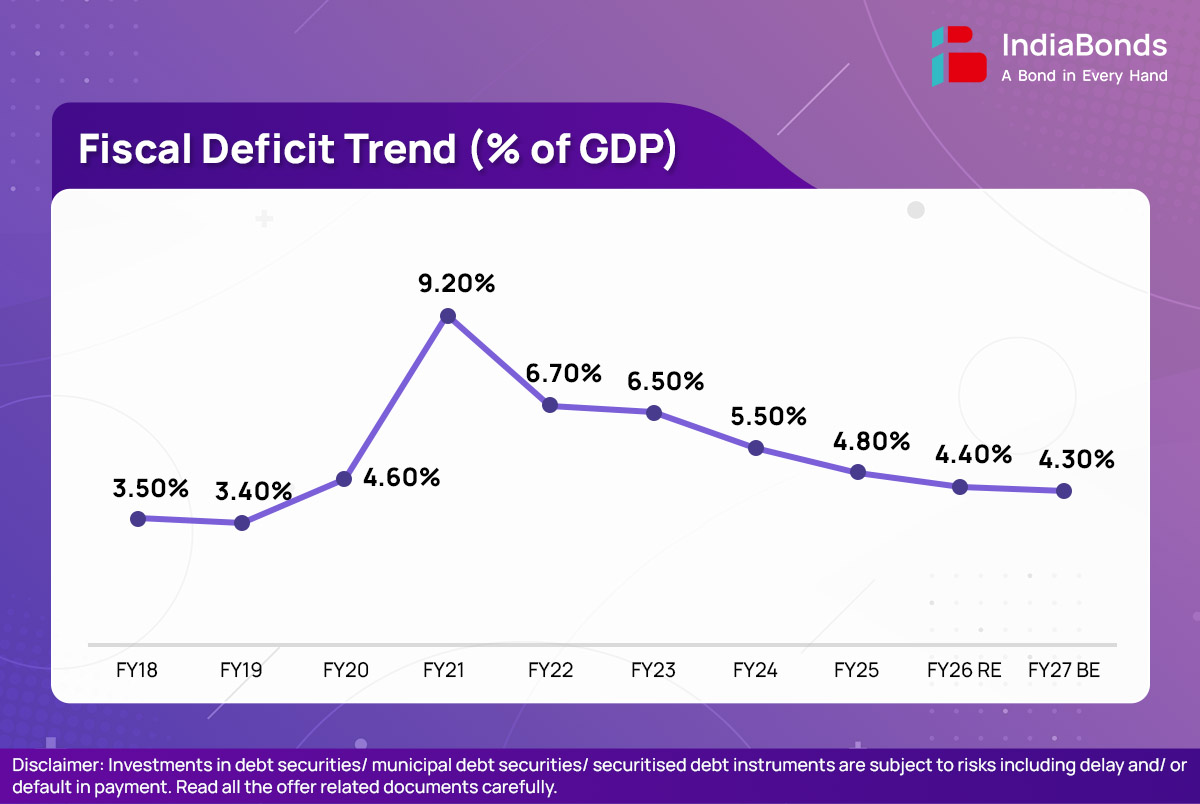

Fiscal Deficit

The government has achieved its budgeted fiscal deficit target for FY25-26 at 4.4% of GDP, thereby meeting the fiscal consolidation objective set in FY20-21 to reduce the deficit below 4.5% by FY25-26. For FY26–27, the government has set a fiscal deficit target of 4.3% of GDP, exceeding market expectations

| Deficit Statistics | ||||

| 2024-2025 Actuals | 2025-2026 BE | 2025-2026 RE | 2026-2027 BE | |

| Fiscal Deficit | 15.74 | 15.69 | 15.58 | 16.96 |

| (4.8) | (4.4) | (4.4) | (4.3) | |

| Revenue Deficit | 5.64 | 5.24 | 5.27 | 5.92 |

| (1.7) | (1.5) | (1.5) | (1.5) | |

| Revenue Receipts | 30.37 | 34.20 | 33.42 | 35.33 |

| Revenue Expenditure | 36.01 | 39.44 | 38.69 | 41.25 |

| Capital Receipts | 16.16 | 16.45 | 16.23 | 18.14 |

| Capital Expenditure | 10.52 | 11.21 | 10.96 | 12.22 |

Notes: Figures in Rs lakh Cr., BE: Budget Estimates, RE: Revised Estimates. Figures in parenthesis are as a percentage of GDP

Budget Estimates 2026-27

◈ Total government expenditure is estimated at ₹ 53.47 lakh crore in FY26-27, compared with revised estimates of ₹ 49.65 lakh crore in FY25-26.

◈ Capital expenditure is projected to maintain strong momentum, with outlays estimated at ₹ 12.22 lakh crore in FY26-27, higher than the revised capital expenditure of ₹ 10.96 lakh crore in FY25-26.

◈ Government’s revenue expenditure is projected at ₹ 41.25 lakh crore, compared to revised

₹ 38.69 lakh crore revenue spending in FY25-26.

◈ Total tax revenue for FY26-27 is estimated at ₹ 28.67 lakh crore, higher than the ₹ 26.75 lakh crore

recorded in FY25-26. The budgeted tax revenue target for FY25-26 was ₹ 28.37 lakh crore.

◈ Non-tax revenue receipt is estimated at ₹ 6.66 lakh crore for FY26-27, compared to revised Rs. 6.67 lakh crore received in FY25-26.

The Path to Fiscal Consolidation

◈ The government has successfully achieved its fiscal consolidation commitment of reducing the fiscal deficit to 4.4% of GDP by FY25–26, as announced in the FY20-21 Budget.

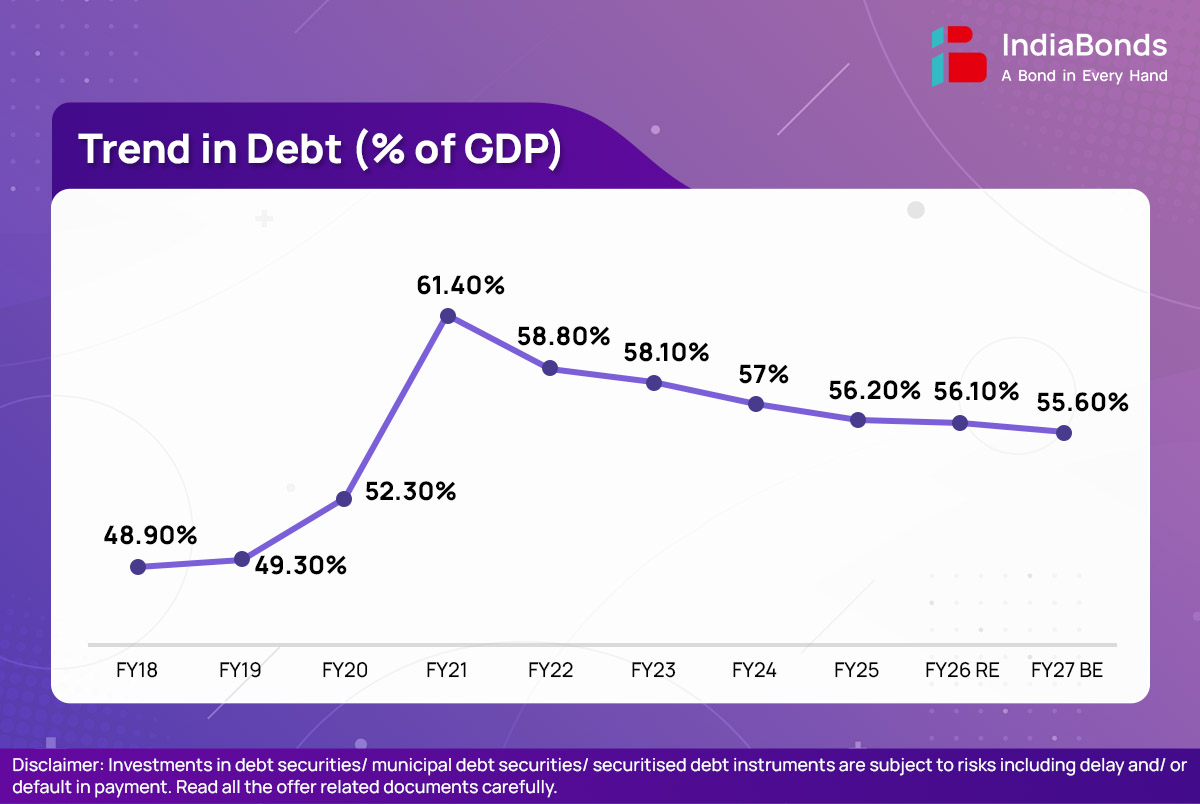

◈ The government has outlined a medium-term objective to gradually reduce the debt-to-GDP ratio to 50% (±1%) by FY30-31, reinforcing its commitment to fiscal sustainability.

◈ The government has targeted a debt-to-GDP of 55.6% in 2026-27 BE, compared to 56.1% of GDP in 2025-26 RE.

| Financial Year | 2024-2025 Actuals | 2025-2026 BE | 2025-2026 RE | 2026-2027 BE |

| Fiscal Deficit % of GDP | 4.8 | 4.4 | 4.4 | 4.3 |

Market Borrowings

◈ Gross market borrowings of the central government are estimated at ₹ 17.20 lakh crore, higher than market expectations and above the ₹ 14.61 lakh crore recorded in FY25-26.

◈ Net market borrowing for FY26-27 is estimated at ₹ 11.73 lakh crore, higher than revised estimates of

₹ 11.33 lakh crore in FY25-26.

◈ The balance financing of fiscal deficit is expected to come from small savings and other sources.

| Financial Year | 2024-2025 Actuals | 2025-2026 BE | 2025-2026 RE | 2026-2027 BE |

| Net Market Borrowing | 11.63 | 11.54 | 11.33 | 11.73 |

(Note: Debt as defined in the FRBM Act includes external debt valued at current exchange rate, and liabilites on account of extra budgetary resources as reported in Statement 27 of Expenditure Profile.)

Financial Sector Reforms & Bond Market Deepening

The budget introduces structural reforms to build a robust and resilient financial sector, essential for efficient capital allocation and risk management

Corporate Bond Market:

To deepen the Corporate Bond Market and improve liquidity, the proposal introduces two key technical enhancements:

◈ Market Making Framework: Establishing a structured framework with improved access to funding and the introduction of derivatives on corporate bond indices to facilitate active trading.

◈ Total Return Swaps (TRS): Introducing total return swaps on corporate bonds to allow investors to exchange the credit and market risk of an underlying bond for a different cash flow, attracting more diverse institutional participants.

Municipal Bonds:

To boost urban infrastructure financing through Municipal Bonds, the proposal introduces a tiered incentive structure:

◈ Large City Incentive: A new ₹100 crore incentive for single bond issuances exceeding

₹1000 crore, aimed at encouraging high-value market borrowing by major metros.

◈ Continued Support for Smaller Towns: Extension of the existing AMRUT scheme to incentivize issuances up to ₹ 200 crore, ensuring smaller and medium towns maintain access to credit markets.

Financial Sector:

To further strengthen the financial sector and align it with future growth goals, the proposal includes the following measures:

◈ Sectoral Health: Recognition of the current banking strength, characterized by historic profitability, improved asset quality, and 98% village coverage.

◈ Banking Sector Review: Establishment of a “High Level Committee on Banking for Viksit Bharat” to conduct a comprehensive review focused on reform-led growth, financial stability, and consumer protection.

◈ NBFC Restructuring: Implementation of a vision for Non-Banking Financial Companies with specific targets for credit and technology. This includes the restructuring of Power Finance Corporation and Rural Electrification Corporation to improve the scale and efficiency of Public Sector NBFCs.

◈ Foreign Investment Reforms: A comprehensive review of FEMA (Non-debt Instruments) Rules to create a more contemporary and user-friendly framework for foreign investors.

Manufacturing: Strategic and frontier sectors

To sustain growth and economic momentum and enhance domestic production and reduce import dependency, scaling up of manufacturing in 7 sectors is emphasized:

◈ Biopharma

◈ Semiconductor

◈ Electronics Components Manufacturing

◈ Rare Earth Corridors

◈ Chemical Production

◈ Capital Goods: Precision component manufacturing, Construction and Infrastructure Equipment (CIE) and Container Manufacturing Scheme

◈ Textile

Creating “Champion SMEs” and supporting micro enterprises

To foster the growth of “Champion SMEs” and support micro-enterprises, this three-pronged strategy integrates Equity Support through a ₹10,000 crore SME Growth Fund and a ₹ 2,000 crore top-up for the Self-Reliant India Fund, alongside Liquidity Support by mandating TReDS for CPSEs, providing credit guarantees, and linking GeM with TReDS for faster financing.

Furthermore, the plan provides Professional Support by deploying “Corporate Mitras”-accredited para-professionals trained by institutions like ICAI and ICSI—to help MSMEs in Tier-II and Tier-III towns navigate compliance affordably.

Public Investment & Infrastructure Financing

Public investment remains a major driver of the economy, with significant implications for lenders and infrastructure finance companies

The infrastructure strategy focuses on the following key pillars:

◈ Public Capex Outlay: Boosting public capex to ₹12.2 lakh crore for FY2026-27 and establishing an Infrastructure Risk Guarantee Fund to provide credit guarantees for private developers.

◈ Urban & Asset Strategy: Prioritizing Tier II and Tier III cities as growth centers and setting up dedicated REITs to monetize and recycle real estate assets held by CPSEs.

◈ Logistics & Freight: Constructing the East- West Dedicated Freight Corridor (Dankuni to Surat) and operationalizing 20 National Waterways, beginning with NW-5 in Odisha.

◈ Maritime Ecosystem: Developing ship repair hubs in Varanasi and Patna, establishing Regional Centres of Excellence for training, and launching a scheme to double the share of coastal and inland cargo to 12% by 2047.

◈ Remote Connectivity: Incentivizing domestic seaplane manufacturing and introducing a Viability Gap Funding (VGF) scheme to support remote operations and tourism.

Urbanization: City Economic Regions

To capitalize on urban growth and regional connectivity, the proposal outlines the following initiatives:

◈ Tier II, Tier III, and Temple-Town Focus: Prioritizing modern infrastructure and basic amenities in emerging growth centres and cultural hubs.

◈ City Economic Regions (CER): Mapping cities based on specific growth drivers with a proposed allocation of ₹ 5,000 crore per CER over 5 years, utilizing a “challenge mode” with reform-cum- results based financing.

◈ High-Speed Rail (HSR) Corridors: Developing seven “growth connectors” to link major cities sustainably.

Energy Security

◈ Total Energy Expenditure: The budget proposes a s ignificant allocation of ₹ 1,09,029 crore for the energy sector in BE 2026-2027.

◈ Decarbonization (CCUS): To align with global climate goals, a roadmap for Carbon Capture Utilization and Storage (CCUS) technologies has been introduced with an outlay of ₹ 20,000 crore over the next five years, targeting sectors like power, steel, and refineries.

◈ T h e bu dge t e m ph as i z e s do m e s t i c manufacturing capacity for renewable energy and storage solutions to fortify the supply chain.

◈ Basic customs duty (BCD) exemptions are extended to capital goods used for manufacturing Lithium-Ion Cells specifically for Battery Energy Storage Systems (BESS), Solar Glass & Clean Fuel Support

Taxation

Direct Taxation

◈ ITR deadlines have been staggered, with returns allowed to be updated until 31 March

◈ An automatic nil-deduction certificate for small taxpayers to reduce unnecessary TDS

◈ Interest awarded by the Motor Accident Claims Tribunal to natural persons will be exempt from income tax

◈ One-time 6-month foreign asset disclosure scheme for small taxpayers to disclose income or assets

Other Tax proposals:

◈ MAT becomes a final tax at a reduced rate of 14%, with restrictions on future credit accumulation but allowing some brought-forward credits

◈ Buybacks for all shareholders will be taxed as capital gains

◈ STT on equity derivatives increased: futures from 0.02% to 0.05%, options from 0.10% to 0.15%

◈ TCS on Liberalised Remittance Scheme (LRS) for educatioN, medical treatment, and overseas tour packages has been significantly reduced to 2%

Key Takeaways from Union budget 2026-27:

The Union Budget 2026-27 can be called a continuation budget that prioritizes long-term fiscal credibility by introducing a new Debt-to-GDP anchor of 50% for the next decade. Its core focus remained on continued infrastructure-led growth while also creating a foundation for the strong manufacturing growth, MSME resilience and urban development in the years to come.

The important takeaways are as follows:

Fiscal Deficit: The government met its long-standing goal of reducing the fiscal deficit to 4.4% of GDP in FY25-26. The FY26-27 target is higher than expected at 4.3%, exceeding market expectations of a more aggressive cut. A formal transition to a Debt-to-GDP anchor (targeting 50% by FY31) signals long-term fiscal sustainability to global rating agencies and bond investors.

Borrowing numbers: While net borrowing of ₹ 11.73 lakh crore is considered manageable, the gross borrowing of ₹17.20 lakh crore is higher than expectations. Yields are expected to remain under pressure in the near term due to this heavy supply. Market participants will now look forward to RBI for liquidity management cues.

Capex & Growth focus: Capital Expenditure is set at ₹ 12.22 lakh crore (over 3% of GDP), continuing the strategy of investment-led growth. Heavy focus on manufacturing in 7 sectors (e.g., Biopharma, Semiconductors, Rare Earths) and development of City Economic Regions (CERs) suggests creation of new growth engines for the long term.

Deepening the Bond & Credit Ecosystem: The budget signals a clear intent to structurally mature the debt markets by focusing on measures to enhance secondary market liquidity and diversify the institutional investor base. Furthermore, there is a strong policy push to institutionalize municipal bonds as a core financing avenue, aiming to make urban centers self-reliant in financing their infrastructure needs.

Taxation: The tax announcements shifted towards enforcement and procedural clarity as the major personal tax and GST rejig were done in the last one year. STT hikes in derivatives indicated continued discomfort among policy makers towards speculative investments.

DISCLAIMER:

Investments in debt securities/ municipal debt securities/ securitized debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. This document does not constitute an offer or recommendation to buy or sell any products or services. The recipients should not act and rely on the information/ data contained in this document for making any investment / any other decision. The information/ data has been sourced from publicly available information.

1.31K

CIN: U67100MH2008PTC178990

SEBI Registration No.: INZ000311637

NSE Member ID - Debt Segment: 90316

BSE Member ID - Debt Segment: 6811

Caution : Beware of fraudsters and impersonators misusing the name of IndiaBonds. Always verify communications and transactions through our official website www.indiabonds.com and mobile application only. Click here for Advisory and Safety Tips.