Blog / Essential / Understanding Bank Bonds in India – Tier 2 & AT1 Bonds

>

Understanding Bank Bonds in India – Tier 2 & AT1 Bonds

What are Bank Bonds?

Banks execute the critical function of lending to institutions and individuals to facilitate cash flow within the financial system. To maintain liquidity, they need large amounts of capital. One way of raising money is through issuing bank bonds in India.

Banks are governed by strict and sound regulations under The Banking Regulation Act, 1949. Further, they come under the supervision and regulatory framework of the apex body i.e. Reserve Bank of India. Globally too, banks need to follow the Basel-III norms which is a worldwide regulatory framework that manages financial stress, maintains market discipline and controls capital adequacy. Over and above this, international or cross-border bank transactions are also governed by law – Foreign Exchange Management Act, 1999.

Since government agencies are constantly monitoring health of banks, it makes the banking sector one of the safest and most regulated sectors. Additionally, the government also owns a majority shareholding in large number of banks in India ensuring their safety in times of stress.

A notable feature of these bonds is that they offer higher returns than bank Fixed Deposit rates, meaning you’ll earn more returns on these bonds than on an FD issued by that same bank one invests in. Please read – Why your parents chose FDs and you may not want to

Bank Bonds and Seniority

Banks, like any company, need to raise money or capital for their business. Given their importance in the economy, they are regulated, need to maintain adequate cash reserves and adequate financial health ratios. Banks raise different types of capital depending on its cost and seniority. Regulators and rating agencies attach different rankings to this capital when calculating a bank’s financial strength.

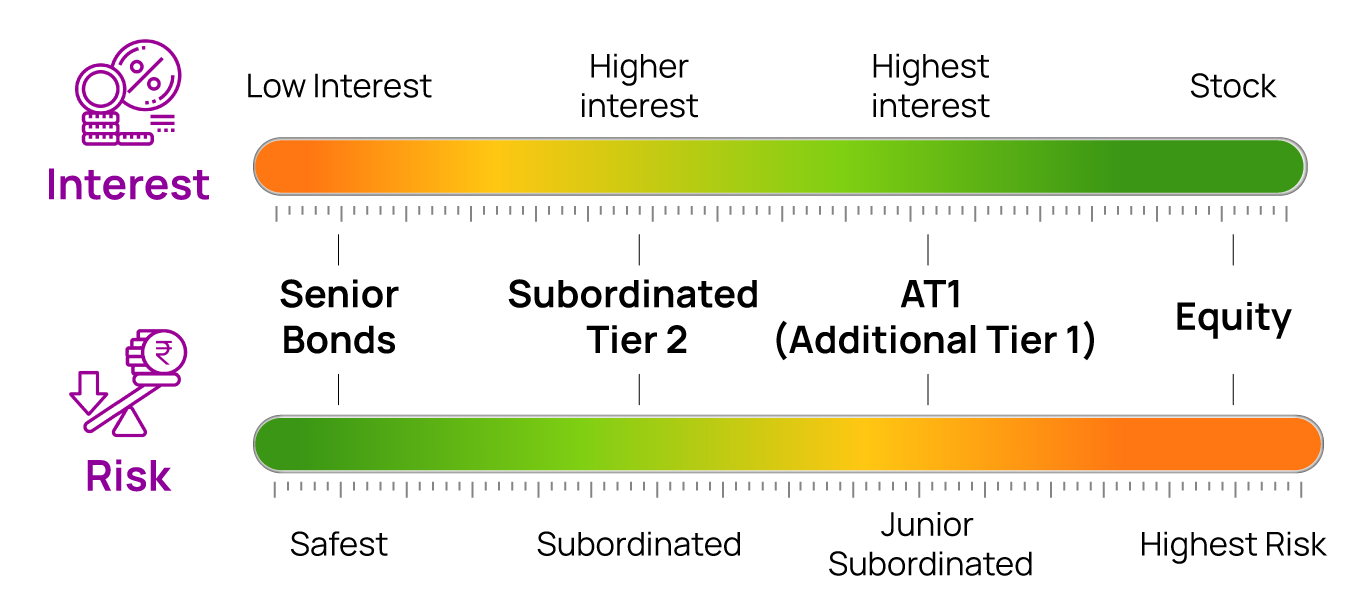

Below is a table of different types of Bank Capital and their seniority (i.e., who gets paid first if a bank was to fall under stress).

Types of Bank Bonds

It is important to understand that there are different types of bank bonds and before investing in them, investors must understand their individual features as well as their seniority ranking. Please remember that all Bank Bonds are not the same. There are broadly three categories of these bonds:

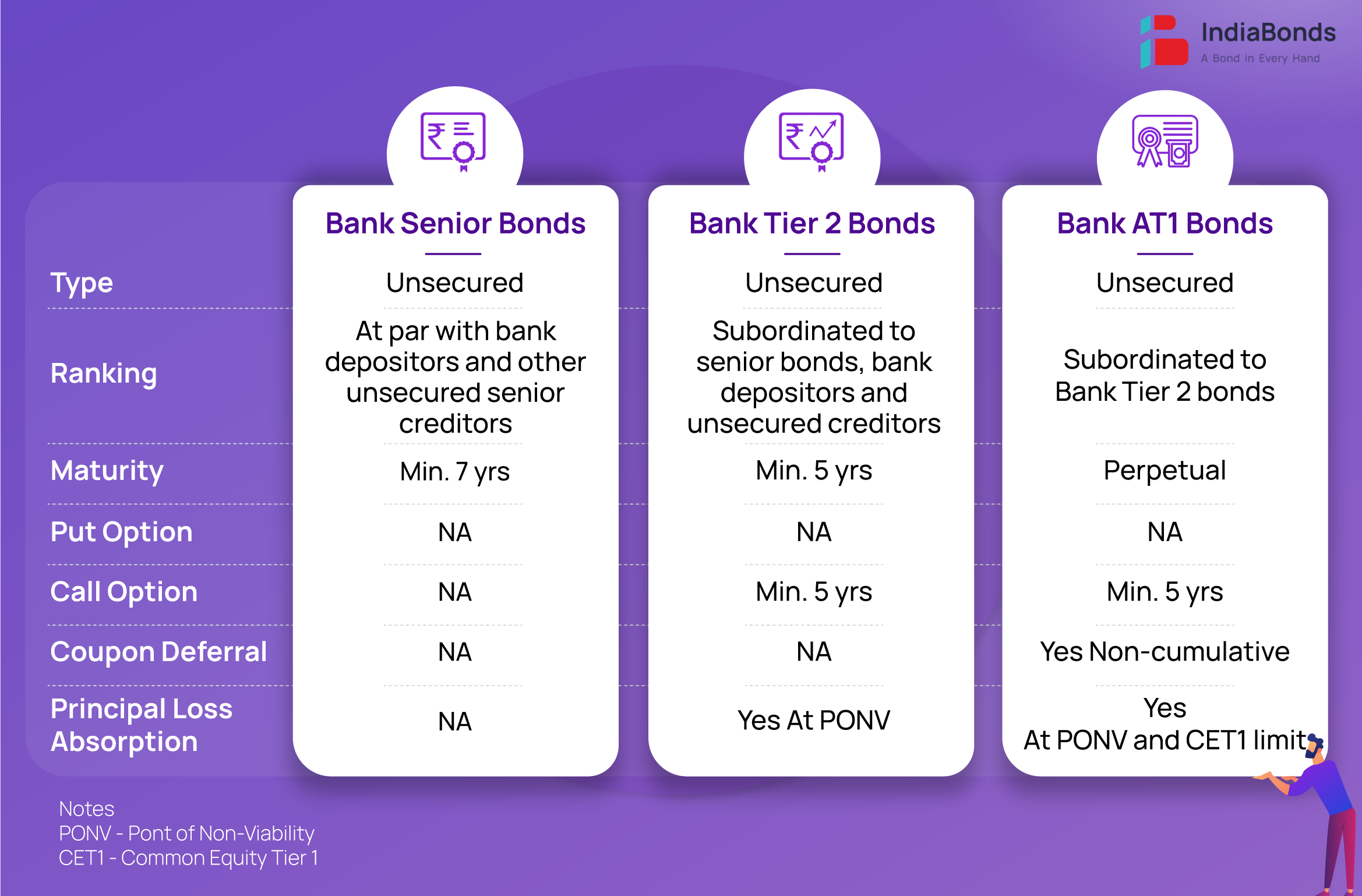

Bank Senior Bonds – Banks can issue senior bonds for Long Term Infrastructure and affordable housing requirements. These have to be for a minimum period of 7 years at the time of issue. Another feature of the bonds is that these are unsecured but are at par with depositors and other uninsured/unsecured creditors of the bank. Furthermore, bank senior bonds do not have any Put or Call Options and have a single bullet redemption or maturity date (no amortization).

Bank Subordinated Tier 2 Bonds – Banks issue Subordinated Tier 2 bonds to meet their Tier 2 capital requirements. These have to be for a minimum period of 5 years at the time of issue. They are unsecured and subordinated in claims to depositors, unsecured creditors and senior bonds of the bank. Bank Tier 2 bonds do not have Put Option and only have a Call Option (option for early repayment) which the bank can exercise after minimum of 5 years and after approval from Reserve Bank of India (RBI). The most important difference of Bank Tier 2 bonds from Bank senior bonds is its loss absorption feature. If a bank is approaching or has approached a point of non-viability (PONV), then RBI can write off the principal amount outstanding on Tier 2 bonds. Essentially bondholders can see their principal written off (partially or wholly) if the bank undergoes financial stress. Hence these bonds pay higher interest rate the bank senior bonds.

Bank AT1 Bonds (Additional Tier 1) – Banks issue AT1 bonds to finance their AT1 capital requirements. These are perpetual (no final maturity), with no Put Option and a minimum 5 years Call Option that can be exercised only after RBI’s approval. Bank AT1 bonds are the junior most amongst these bonds, are unsecured, subordinated even to Bank Tier 2 bonds and senior only to a bank’s equity in ranking. Of course, bank depositors and other unsecured creditors rank much higher than the Bank AT1 bondholders in times of financial stress. The loss absorption features of Bank AT1 Bonds go even a step further than the Bank Tier 2 Bonds. Here too RBI can write off the principal outstanding on AT1 Bonds if the bank is approaching or has approached point of non-viability (PONV). In addition, the principal amount of Bank AT1 Bonds can be temporarily written down or even permanently written off if the Common Equity Tier 1 (CET1) ration of the bank falls below the minimum regulatory prescribed threshold limit. Also, interest payment on Bank AT1 Bonds can only be made out of distributable income of the bank and is also subject to the bank meeting its minimum capital adequacy requirements. Any such interest foregone is non-cumulative in nature (cannot be reclaimed in future).

A quick table below that compares the different types of Bank Bonds:

Summary:

In brief, all Bank Bonds are not the same and it is important for investors to understand the structural differences between them. There is a reason why some bonds issued by the same bank pay more interest than others. In recent financial history of India, we have seen some Bank AT1s prepaid at par whilst others been written off too! Hence, knowledge is power. To know more and explore your investment options in these Bonds, you can view offerings from IndiaBonds here EXPLORE

Disclaimer: Investments in debt securities/ municipal debt securities/ securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully.

<

Previous Blog

Online Bond Yield Calculator – Simplifying Bond Yield and Bond Price

Next Blog

What are 54EC Bonds or Capital Gain Bonds

>

Table of Contents

Bonds you may like...

MAHAVEER FINANCE (INDIA) LIMITED

Coupon

12.4000%

Maturity

Sep 2031

Rating

CRISIL BBB+

Type of Bond

RBI Repo Rate + 7.15% Spread

Yield

13.0000%

Price

₹ 1,00,613.84

PROGFIN PRIVATE LIMITED

Coupon

10.5000%

Maturity

Dec 2027

Rating

ICRA BBB+

Type of Bond

Secured - Regular Bond/Debenture

Yield

11.9000%

Price

₹ 99,286.04

SPANDANA SPHOORTY FINANCIAL LIMITED

Coupon

11.2500%

Maturity

Apr 2028

Rating

ICRA BBB+

Type of Bond

Secured - Regular Bond/Debenture

Yield

11.7500%

Price

₹ 10,034.56

FINNABLE CREDIT PRIVATE LIMITED

Coupon

11.0000%

Maturity

Sep 2028

Rating

CARE BBB+

Type of Bond

Secured - Regular Bond/Debenture

Yield

11.5500%

Price

₹ 1,00,278.33

FINNABLE CREDIT PRIVATE LIMITED

Coupon

11.1000%

Maturity

Jul 2029

Rating

CARE BBB+

Type of Bond

Secured - Regular Bond/Debenture

Yield

11.5500%

Price

₹ 1,00,459.30

FINNABLE CREDIT PRIVATE LIMITED

Coupon

11.0000%

Maturity

Aug 2028

Rating

CARE BBB+

Type of Bond

Secured - Regular Bond/Debenture

Yield

11.5500%

Price

₹ 10,027.75

NAMRA FINANCE LIMITED

Coupon

11.2500%

Maturity

Sep 2028

Rating

ACUITE A-

Type of Bond

Secured - Regular Bond/Debenture

Yield

11.5200%

Price

₹ 1,01,957.08

ESAF SMALL FINANCE BANK LIMITED

Coupon

11.6500%

Maturity

Jul 2032

Rating

CARE A-

Type of Bond

Subordinate Debt Tier 2 - Lower

Yield

11.4500%

Price

₹ 1,04,094.71

Note:

The listing of products above should not be considered an endorsement or recommendation to invest. Please use your own discretion before you transact. The listed products and their price or yield are subject to availability and market cutoff times. Pursuant to the provisions of Section 193 of Income Tax Act, 1961, as amended, with effect from, 1st April 2023, TDS will be deducted @ 10% on any interest payable on any security issued by a company (i.e. securities other than securities issued by the Central Government or a State Government).

Note: The listing of products above should not be considered an endorsement or recommendation to invest. Please use your own discretion before you transact. The listed products and their price or yield are subject to availability and market cutoff times. Pursuant to the provisions of Section 193 of Income Tax Act, 1961, as amended, with effect from, 1st April 2023, TDS will be deducted @ 10% on any interest payable on any security issued by a company (i.e. securities other than securities issued by the Central Government or a State Government).

16.15K

16.15K